- Home

- Meet Concordia

- Admissions

- Admissions 2026

- Preparatory Department

- Tuition Fee

- Admission for Bachelor Degrees

- Admission for Master Degrees

- Admission for Ph.D. Degree

- International Students Enrollment

- In-service Training

- Admissions Office

- Scholarships

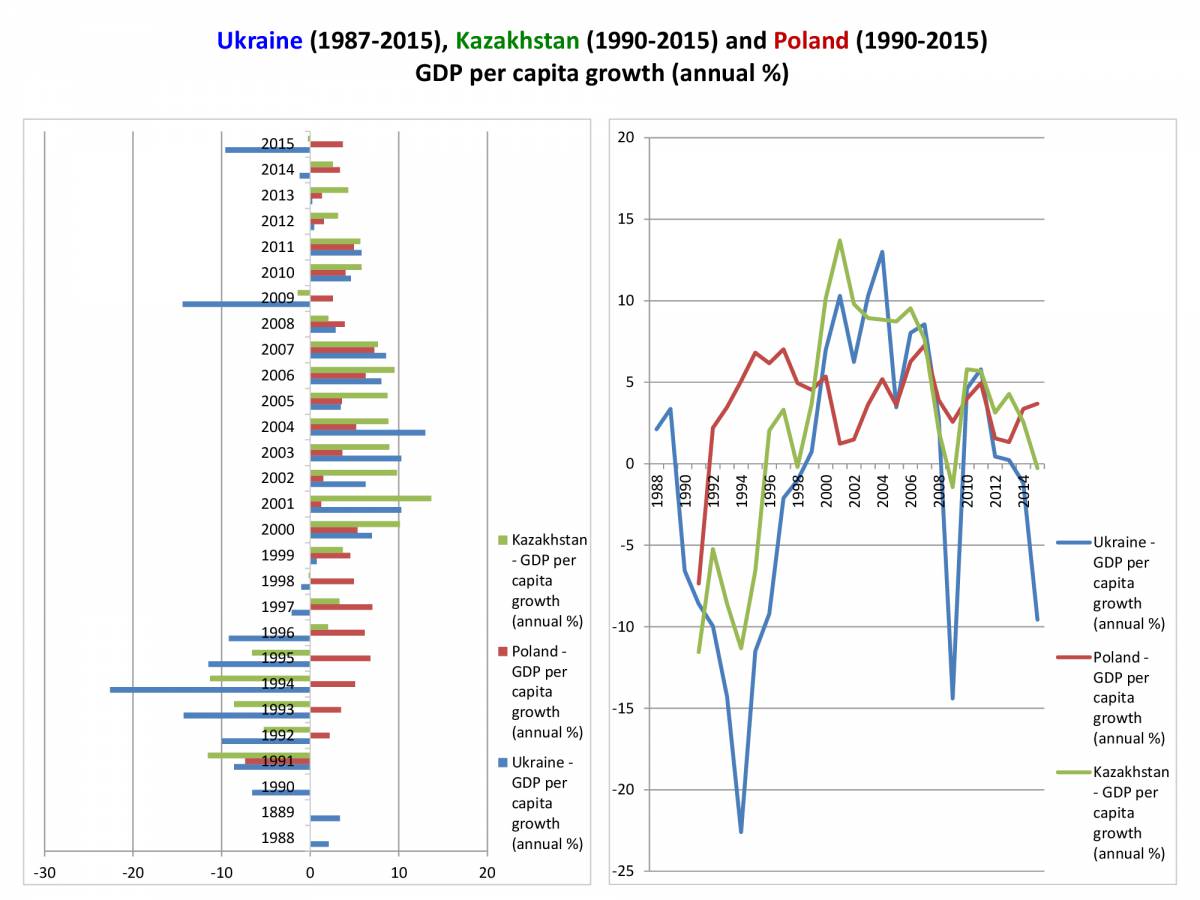

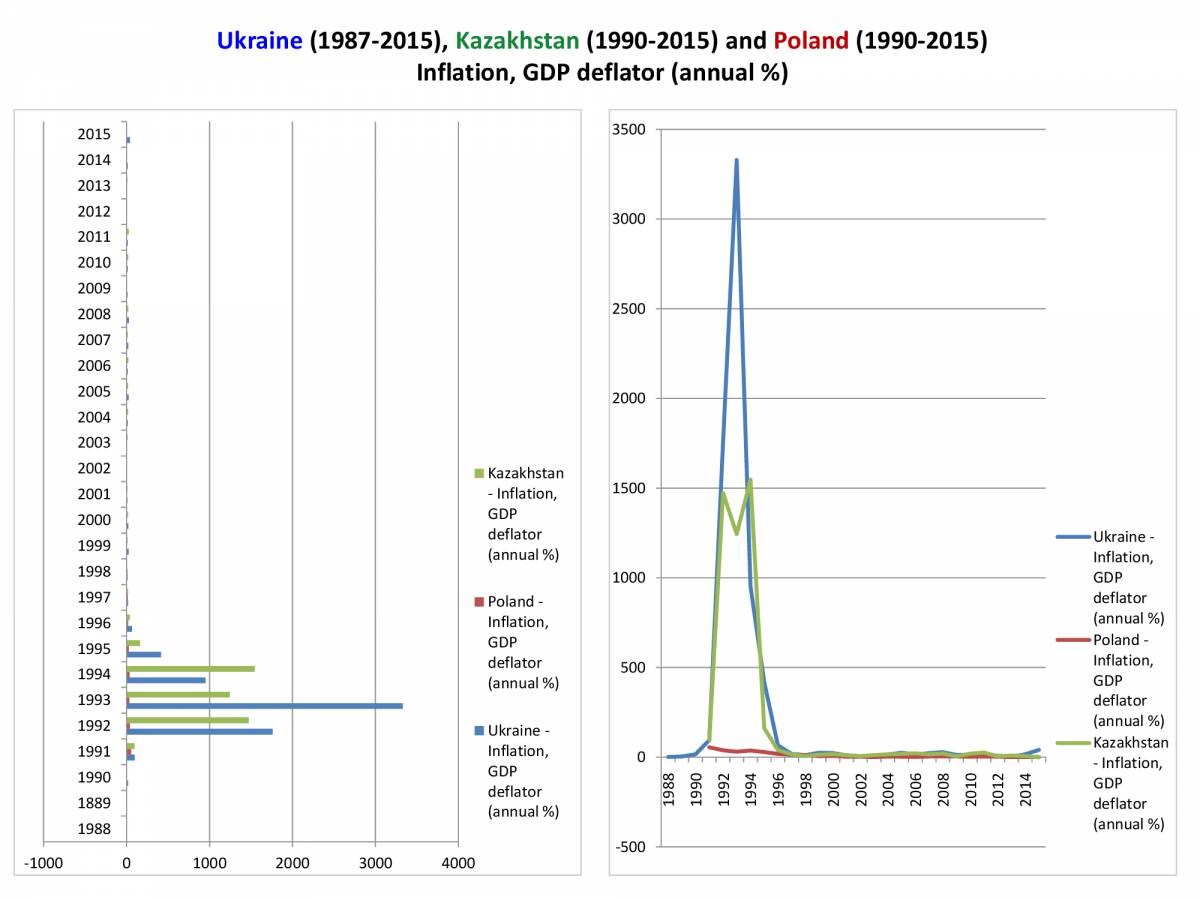

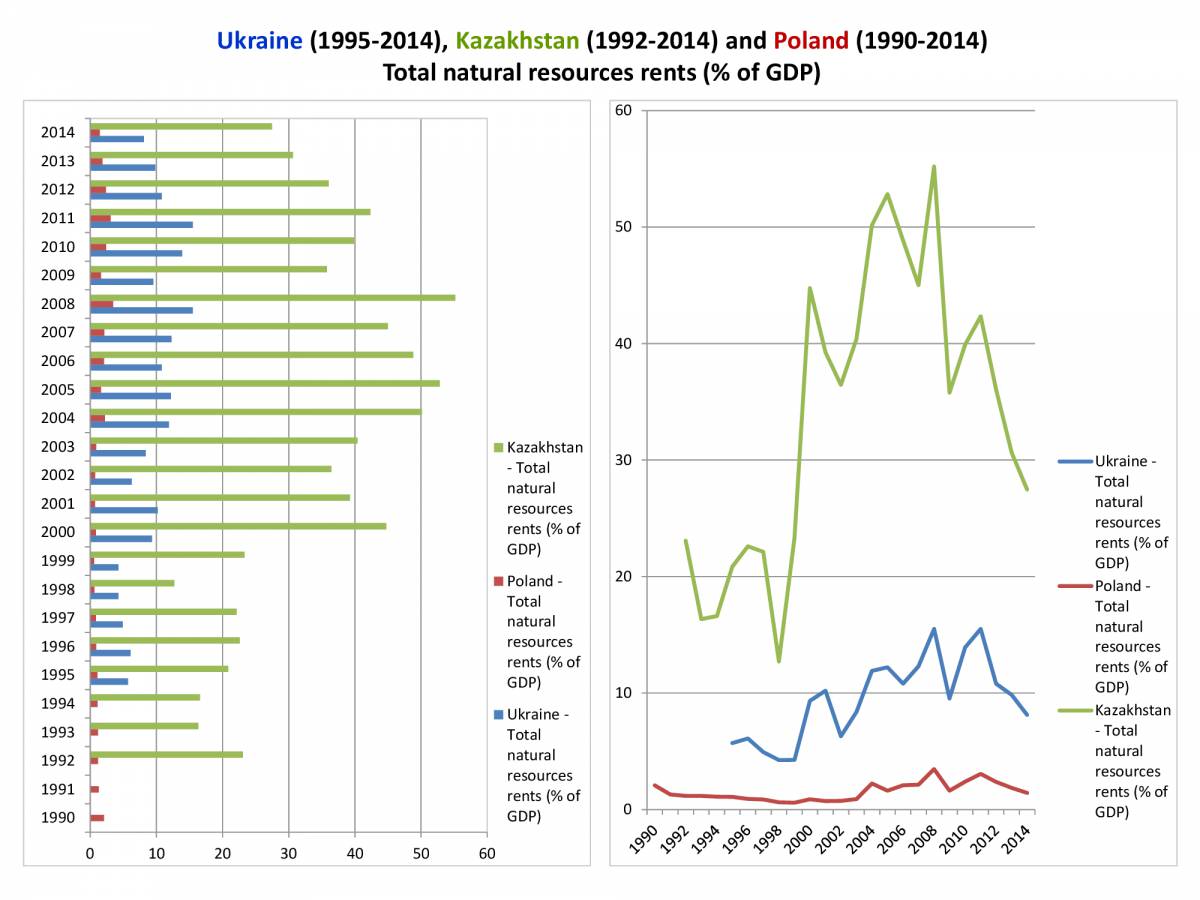

- ConcordiaUA Presentation

- General Data Protection Regulation (GDPR)

- Regulations of the Ministry of Education and Science

- Academics

- Career

- Apply Now!